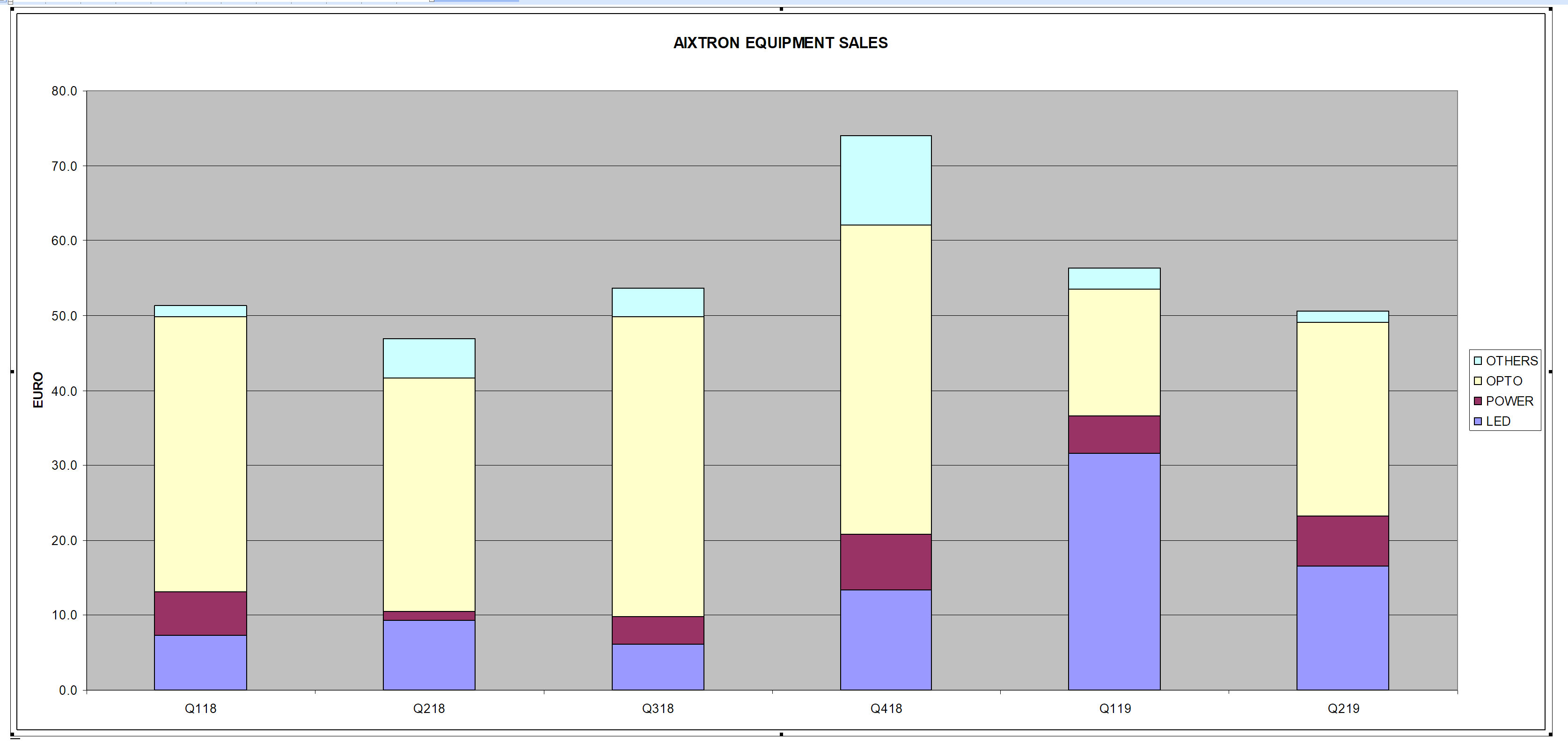

This breakdown reveals Aixtron's businesses over the last 6 Q's.

1. Opto (VCSEL) saved Aixtron. Without it, the company would have been in bad shape. It has declined from Q418, but possibly climbing back. VCSEL is critical to Aixtron. New VCSEL applications like Time-Of-Flight (TOF) for rear camera and Augmented Reality (AR) in iPhones and Android phones, auto, LIDAR, etc. may propel new wave of MOCVD orders.

2. Power segment MOCVD sales have been tiny. Only a few million euros per Q and no sign of acceleration (yet). That's only one or two MOCVD per Q only. That also means when this segment turns hot, the sales could easily double and triple per Q. Looking around for applications in 5G which the demand of MOCVD for GaAs, GaN-on-Si and GaN-on-SiC, SiC for EV, fast charging devices for phones, etc. should be in good.

3 LED is still very important. It is over 10 million over the last few Q's. SanAn, PlayNitride, Epistar, etc. are aggressively moving into mini and micro LED. PlayNitride is starting production this September and I think they have five G5 already based on DigiTimes story. LED for UV applications may also be picking steam.

4 Others, the research equipment such as black magic and the new small R&D MOCVD can sometimes make a difference. Aixtron had 12 million sales in Q418.

To meet the 2019 guidance, Aixtron needs to sell 116 million of equipment in Q3 and Q4. I am thinking Aixtron needs to sell 20 million LED, 35m Power, 55m Opto and 6m others, to make up the 116m. The whole picture would depend on the speed of increase of Power and Opto applications. If OLED can add 10m or so, that would be good. |

Angehängte Grafik:

aixtron_equipment_sales.png (verkleinert auf 15%)

Thread abonnieren

Thread abonnieren

baggo-mh

baggo-mh