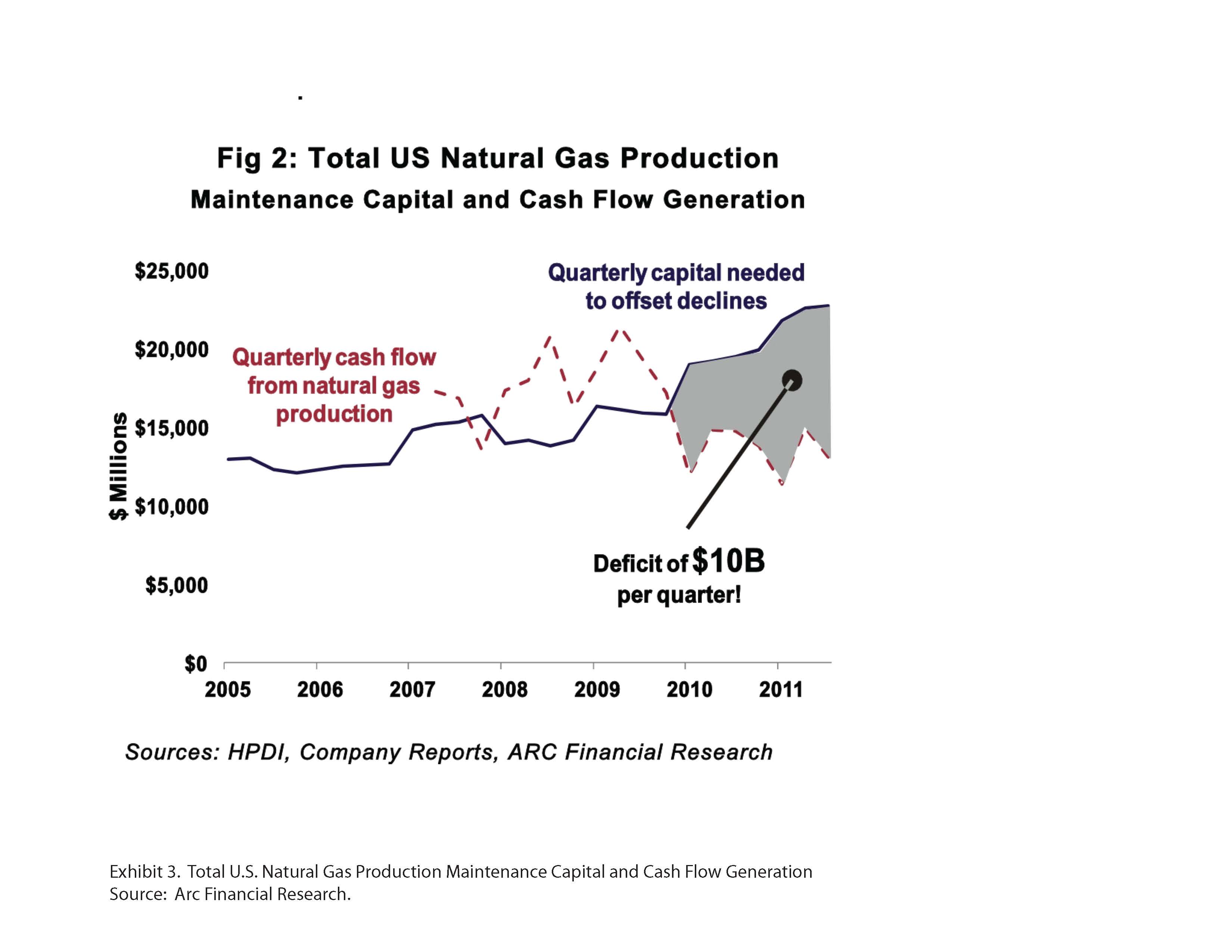

http://www.theoildrum.com/node/8914 Conclusions A secular shift has occurred in the U.S. domestic gas supply by drilling mostly shale formations, formerly considered source rocks too costly to develop. The tremendous number of wells drilled in the last several years has contributed to an over-supply of gas. The shale revolution did not begin because producing oil and gas from shale was a good idea but because more attractive opportunities were largely exhausted. Initial production rates from shale are high but expensive drilling and completion costs make economics challenging. The gold rush mentality taken by companies to enter shale plays has added expensive leases and new pipelines to those costs, further complicating shale gas economics. In the decades before shale plays, the exploration and production emphasis was on discipline. Science was used to identify the most prospective areas in order to limit the amount of acreage to be acquired and its cost. Shale plays have produced a land grab business model in which hundreds of thousands of acres are acquired by each company. Unprecedented lease costs have become the norm often based on limited information and science. Operators have indulged in over-drilling these plays for many reasons but adding reserves, holding leases and company growth are among the main factors particularly with the low cost of capital. The inevitable result has been the collapse of prices as supply exceeded demand. Most analysts forecast that the future will be much like the present, and that natural gas will be abundant and cheap for decades to come. There are, however, strong and consistent indicators that natural gas supply may be less certain than most observers believe and require a higher price to be developed economically. Natural gas demand is growing as fuel switching for electric power generation continues, and will be increased by environmental regulation in the coming years. The U.S. will shift more of its future energy needs to natural gas in many sectors of the economy. The best justification, in fact, for the land grab and over-drilling spree is expectation of higher prices. Those companies that grabbed the land and held it by production will profit greatly once the true supply and cost of shale gas is recognized. The financial survival of all companies in this position is not, however, certain. Price matters, and there is finally some response from shale gas producers with recent announcements to curtail drilling. While price was cited as the main reason for reduced drilling, it is likely that some companies now have financial constraints. The shale gas phenomenon has been funded mostly by debt and equity offerings. At this point, further debt and share dilution are less feasible for many companies. Joint ventures have provided a way for some to prolong spending but that now seems like a less likely source of funding. Capital availability in the near term will likely be tighter than is has until now. Acquisition and consolidation may become more attractive to companies with cash as producers become more extended. Some of the shale gas plays may be at or near peak production at least at the current price of gas and technology. All major producing areas except Louisiana are in decline. Some doubt the accuracy of public data compared with EIA data, but it seems unlikely that the trends it shows are erroneous. In any case, the data the EIA makes available does not have sufficient resolution to evaluate individual plays or state-level trends. Intermediate-term shale well performance is poorer than assumed previously . Continuous treadmill drilling masks this issue so play decline rates are not recognized. High decline rates are, however, a salient issue meaning that and most of a shale gas well's reserve is produced in the first few years. Well life appears to be shorter than initial expectations. This means that an increasing number of wells must be drilled in order to maintain supply. Now, it appears that fewer wells may be drilled until price recovers to commercial levels. The argument for improved efficiency that cites increasing production with lower rig count is suspect. It is mostly because of the large backlog of previously drilled wells that are just now being connected to sales. This spare capacity provides a boost to supply during a period of falling gas-directed rig count. The gold rush is over at least for now for the less commercial shale plays. The money and activity have moved to more oil-prone shale plays such as the Eagle Ford and Bakken or to higher potential gas plays such as the Marcellus. Improbable stories that great profits can be made at increasingly lower prices have intersected with reality. A painful adjustment is underway in the natural gas exploration and production industry. Fewer jobs will be created and projects may develop more slowly. This development may expose the notion of long-term natural gas abundance and cheap gas as an illusion. The good news is that this adjustment will lead to higher gas prices in a future less distant than most believe. Higher prices coupled with greater discipline in drilling will allow operators to earn a suitable return and offer the best opportunity for supply to grow to meet future needs. References Andreoli, D., 2011, The Bakken Boom - A Modern-Day Gold Rush. The Oil Drum: http://www.theoildrum.com/node/8697. Berman, A.E. and L. Pittinger, 2011, U.S. Shale Gas: Less Abundance, Higher Cost. The Oil Drum: http://www.theoildrum.com/node/8212. EIA Annual Energy Outlook 2011 Early Release Overview. EIA Annual Energy Outlook 2011 Natural Gas Tables: http://www.eia.gov/oiaf/aeo/tablebrowser/...Y2012&subject=0-EA.... Gilbert, D. and R. Dezember, Chesapeake Energy Pulls Back Amid Natural-Gas Glut: Wall Street Journal, January 24, 2011:http://online.wsj.com/article/...405297020380650457717865173251197.... Potential Gas Committee 2010 Report: http://www.potentialgas.org/. |

Thread abonnieren

Thread abonnieren

{kind=link}