....

The Obama administration has vowed for CO2 reduction of 28% by 2025 and 32% by 2030, from 2005 levels. This version turns out to be a little stronger than the draft proposal released last summer wherein the EPA had proposed total CO2 reduction of 29% by 2025 and 30% by 2030.

The plan sets carbon pollution reduction goals for power plants and requires states to implement plans to meet these goals. States have until Sep 2016 to submit plans, but all must comply by 2022.

Obama faces stiff opposition on climate issues from the Republicans in the Congress. The Republicans contend that the climate change deal will be economically damaging for the U.S. economy, middle-class families and struggling miners. Coal mining states such as Wyoming, West Virginia and Kentucky fear that their economies would suffer and people would be laid off.... Obama brushed off the notion that his plan was a "War on Coal" ruthlessly killing jobs. The President said that he is reinvesting in areas of the U.S. previously known as "coal country."

.....

Although it’s debatable whether Obama's broader climate plan can solve climate change, this is certainly one of the most historic and ambitious climate rules, given that power plants account for 31% of U.S. greenhouse gas emissions. The Clean Power Plan has unmistakably put renewable energy companies in sharp focus.

Sunedison,Sunpower ...

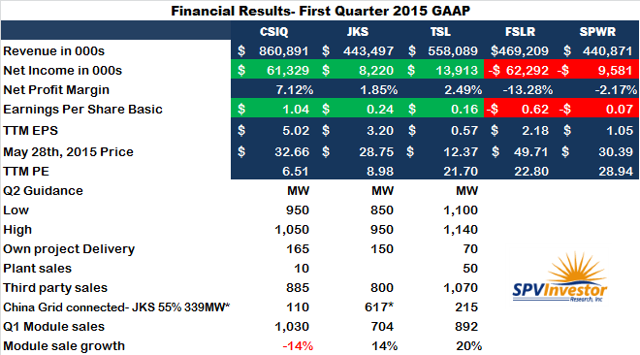

Canadian Solar Inc. CSIQ

Canadian Solar caters to a geographically diverse customer base spread across key markets in the U.S., Canada and Europe, as well as emerging markets like South Korea, Singapore and Brazil. The company, which has a strong pipeline of projects, continues to engage in acquisitions and adopt various strategies to further consolidate its position. During the first quarter of 2015, it acquired Recurrent Energy, LLC, a leading North American solar energy developer, thereby strengthening its hold in the business of ownership and development of solar power plants in North America.

Canadian Solar presently holds a Zacks Rank #3 (Hold) and is trading at a forward PE of 11.34x.

|

Thread abonnieren

Thread abonnieren

{kind=link}